*Editor’s Note: Keep up to date on all things Valuation World Cup here!

Group B – Major Upset, Major Metrics

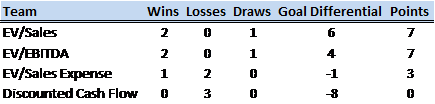

And the first powerhouse is out! The Group of Death was too much for the Discounted Cash Flow method. But with the seeming favorite out, how did the other metrics play out?

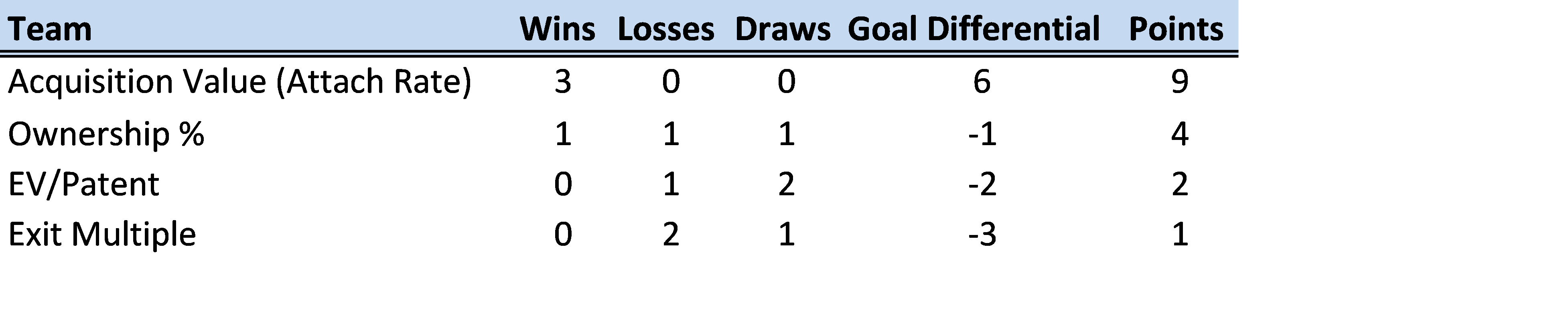

EV/Sales and EV/EBITDA advance!

Game 1: Enterprise Value/Sales 5-1 Discounted Cash Flow

Game 2: Enterprise Value/EBITDA 3-2 Enterprise Value/Sales Expense

Game 3: Enterprise Value/Sales Expense 2-0 Discounted Cash Flow

Game 4: Enterprise Value/EBITDA 2-2 Enterprise Value/Sales

Game 5: Discounted Cash Flow 0-3 Enterprise Value/EBITDA

Game 6: Enterprise Value/Sales 3-1 Enterprise Value/Sales Expense

Closest Match

With only one draw in the group, it’s evident that EV/Sales and EV/EBITDA are contenders at the top of their games. Both have the strength to go deep in the tournament… perhaps looking reminiscent of Brazil and Mexico in that other World Cup, especially if El Tri can keep getting performances like that out of Ochoa! But we digress. Let’s look at these metrics’ respective advantages:

For the EV/Sales multiple, it’s about simplicity. You can approach a company with negative cash flows and still capture the majority of the growth potential as an investor. It’s also much easier to project revenue than revenue and a full cost structure. Fewer variables to get wrong means a clearer picture of expected value. It’s like having one superstar who you can count on for at least a goal a game (re: Neymar, Messi).

EV/EBITDA takes a more complete approach to valuation, considering the cost of doing business which can vary significantly between even similar business models. It also doesn’t get bogged down in non-cash expenses or potential tax breaks, like the DCF or even the disqualified EV/Earnings. It’s like a long-lost love child of EV/Sales and EV/Sales Expense, à la Czechoslovakia, except this combo’s still kicking!

Biggest Blow Out

Discounted Cash Flow took an early walloping from EV/Sales, and was never the same. In our Group B preview, we compared the complexity of the DCF model to the Spanish tiki-taka futbol… little did we realize we had made two bold predictions in one! Realistically, the DCF was simply out of its element. Just think – precision passing and team-focused play led the Spurs to an NBA Championship but came up short for Spain in the World Cup.1 In this bracket, as in the Spaniard’s loss, simplicity is beautiful:

Memorable Moment

EV/Sales Expense thought their claim as the only measure that took into account the cost-per-sale metric might be defensible. But during their head-to-head with EV/EBITDA they looked about as lost as Mr. Yoshida trying to defend James Rodríguez…

1Spain seems to be one of the only World Cup countries not represented on the Spurs’ 15-man roster: Argentina, Australia (twice), Brazil, France (twice), Italy, and the United States.