This is my first run at a teardown of a Series A Company.

I am going to try to make this a recurring theme where I dive into a publicly available Company pitch deck and derive an investment and due diligence memo from it.

Why? Because as a VC-nerd I find this fun but I aware I probably need more hobbies 🙂 In reality, I hope this can provide a framework into how I look at certain types of companies in various sectors.

Company: Front

Website: https://frontapp.com/

Front Original Slide Deck – Series A, 2016

Key Takeaway

- A promising company with solid initial traction and potential to warrant a continued look.

Company Description

- Front is a collaboration tool for enterprises. It is a multi-channel email system that provides a unified view and allows teams to collaborate across the enterprise.

What could make Front a success? What could make it struggle to succeed?

- Front has good initial traction and has been very capital efficient since inception. This financial rigor combined with an ability to scale and generate consistent growth could allow them to achieve a sizeable outcome.

- Front could struggle if they cannot transition from organic growth to paid growth to effectively reach scale and if other major players in the communication space decide to build a competing product.

Market Potential

- If executed properly, Front has the potential to take share from the external communications, support, and customer service industries, a billion dollar business is feasible.

Management Team

- The Head of Sales is the former 1st salesperson at Box and the Head of Customer success was head of upsells at Dropbox. This seems to be a quality team for entering the market.

Investors/Financing

- Front participated in Y combinator and then raised a $3M Seed round in 2014 from notable angels including Elad Gil, Dave Morin, Alexis Ohanian, and Paul Buchheit.

Competition

- Combination of established players and growth stage/VC backed companies

Customers

- Front has signed up a few major brands and other lighthouse customers but the extent of their revenue concentration from these customers is unknown. I would want to understand more about how much MRR these select customers were responsible for before passing judgement on whether these are true customers or just marketing ploys.

Financials/Growth/KPIs/Business Model

Pricing

- For the sake of this exercise, I am assuming that pricing hasn’t changed since 2016 from what is on the current website.

- This is clearly a high volume, low price per user business. The company employs a land and expand strategy where they sign up individuals and small teams and then look to upsell and cross-sell to the rest of the organization.

- Bonus points for the 14 day free trial as well as the annual pricing with the 17% savings highlighted as each plan is billed annually upon sign up resulting in cash inflow from day 1 as opposed to monthly. This sales incentive to generate cash flow is part of the Company’s financial rigor that I am impressed with.

MRR and Customer Count

- The company has shown consistent and impressive MRR growth and increased customer adoption. This is excellent to see this consistent early traction with no marketing spend

- That said, doing an estimated MRR per customer shows a different story. As seen below, the average MRR per customer shows a continued decline. While it is great they are growing both MRR and customers, it appears that the average MRR per customer is decreasing each month meaning that less and less seats are signing up per new customer.

| Estimated MRR, Customer Count | |||

| Date | MRR | Company Count | Avg. MRR per Customer |

| 9/1/14 | $15,000 | 62 | $242 |

| 12/1/14 | $26,000 | 125 | $208 |

| 3/1/15 | $41,000 | 200 | $205 |

| 6/1/15 | $59,000 | 330 | $179 |

| 9/1/15 | $82,000 | 500 | $164 |

| 12/1/15 | $97,500 | 670 | $146 |

| 3/1/16 | $113,000 | 880 | $128 |

| *my estimated calculations by reading the graph in more detail | |||

- I would continue to monitor this trend as it could be a sign of trouble should the average keep getting lower and lower. I understand that this is a freemium/self-service type SaaS model with low barriers to adoption but this is something that worries me especially for when they have to move to paid advertising to attract customers and the resulting LTV/CAC ratio could be based on drastically lower LTV expectations.

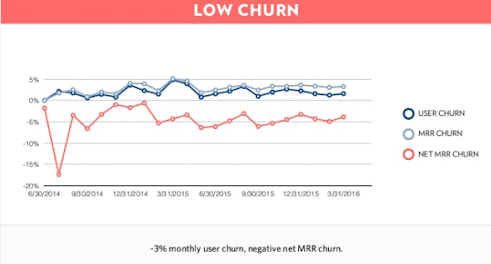

User Churn

- Front advertises low churn and negative net MRR churn. While the negative dollar churn appears to be true, the 3% monthly user churn seems a bit high to me as that annualizes out to about 31% user churn which at 1000 customers would be 310 lost customers a year! I understand that this is a high volume business but that is a dangerous amount of customers to lose even at this early stage.

- I would want to learn more from management as to the main causes of churn

Dollar Churn

- On the flip side, I am impressed with their successful expansion strategy and the resulting negative net MRR dollar churn. The ability for the company to replace not only the dollars lost from the churned users through greatly expanding MRR from retained customers has been very impressive. Especially impressive has been the ability to continually increase the MRR on an annual cohort basis of 150% of starting MRR. This helps prove their product is not only viable for its initial customers but that Front can successfully upsell consistently over time.

- Conversely, if my calculations on average MRR per customer are correct, the absolute dollar value of MRR expansion may not be as impressive on the more recent cohorts. Seeing that Average MRR per customer has decreased from ~$240 to ~$130 since the cohort measurements started, getting to 150% annual expansion of $130 MRR would only generate $195 in MRR so the expansion of a lower starting MRR customer is less impressive on a percentage basis. While it is nice to see that they can land and expand, if the starting point continues to get smaller it may be a cause for concern.

- I would want to ask management more about their customer dynamics around free trial conversions, customer revenue concentration within each cohort, and expansion strategy playbook.

Capital Efficiency

- To me, this is where Front shines. The fact that they have only spent $1.3M to arrive at $1.4M in ARR is extremely impressive especially given how much companies are spending on customer acquisition, engineering talent, and perks these days.

- The other impressive piece is they still have over half of their Seed round left. That and their $90k monthly burn rate gives them about 20 months of runway so even without this $10M they are still on solid financial footing.

Projections

- Front expects to triple ARR in 2017 and while this would be impressive, it is unclear where that sales efficiency would come from based on this financial plan. I would want to ask management a lot more questions around how they plan to build up this ARR and what the “Other” expense entailed as it is unclear if this is salary for sales, rent for a building, etc.

- The non-engineering spend seems to taper off starting in February 2017 so it appears they expect to hire aggressively through the end of 2016 but less so in 2017. I would be curious to know their hiring plans as well as their sales and marketing plans.

Valuation

- According to Pitchbook, the Company raised their $10M at $30M pre for a post-money valuation of $40M. While I am unsure the validity of these terms, this could be an appropriate valuation for the round given the Company traction. While you can’t really use public company multiples as a comparison given the differences in company profile, a few other methods could give us comfort.

VC Ownership Method

- From a venture ownership, this follows the more traditional model of investors owning ~25% of a company in the series A so that isn’t out of the ordinary and what i believe had an outsized influence on this valuation and pricing of the round.

VC Rate of Return Method:

- If Front raised $10M, Series A investors would expect a $100M return (10x) which would be $400M in exit value which in the realm of B2B SaaS deals is more than reasonable. With major corporations spending hundreds of millions and even billions in M&A each year combined with the ability for companies to IPO at the $100M revenue threshold on a path to profitability, the options for an exit of this caliber are fathomable if Front can execute on their vision long term.

Conclusion:

- Front’s value proposition, its capital efficient growth, and capable management team have demonstrated enough value to warrant a sizeable uptick in valuation from their seed round. I recommend we continue further diligence with management.

Disclosure: My employer (SVB) may do business or seek to do business with companies mentioned or their competitors. Views expressed above are solely the views of me.